Small Business Deductions and Limits You Need to Know in 2025 and 2026

- Contributor

- Debbie Alexander

Nov 28, 2025

The Senate Finance Committee claims that the One Big Beautiful Bill Act (OBBBA) delivers “targeted relief to America’s small businesses.”

Is this statement true?

Let’s go over what the OBBBA has changed for small businesses so that you know exactly what tax-saving opportunities you have as we move into 2026. In this article, we’re going to answer the following questions:

- What deductions/credits/incentives were created, extended, or enhanced with the OBBBA?

- What are the new thresholds that small businesses need to think about in 2025 and 2026?

What deductions/credits/incentives were extended or enhanced with the OBBBA?

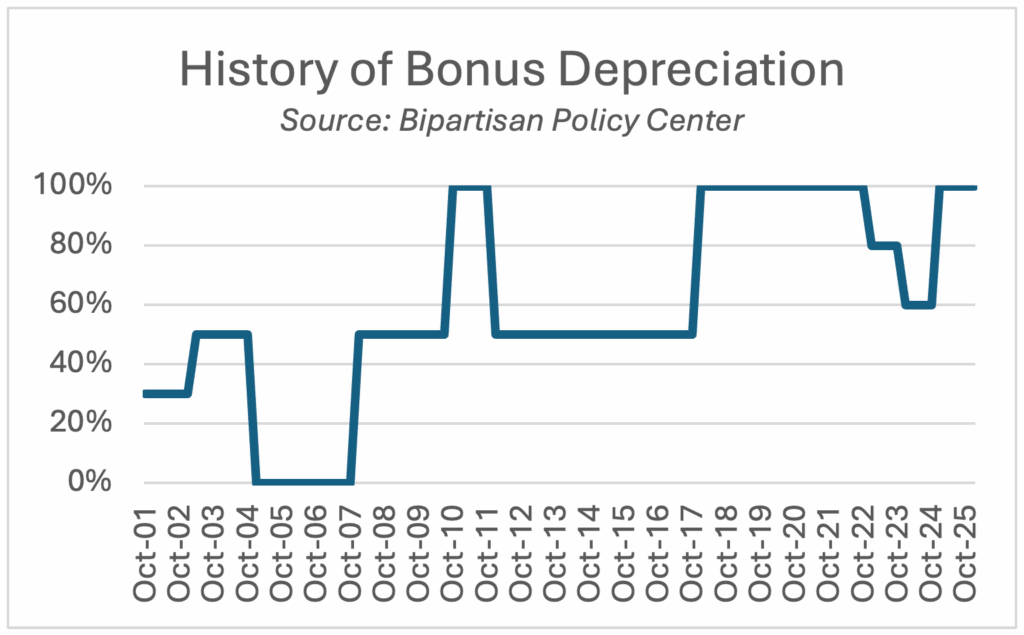

Reinstated 100% Bonus Depreciation

The OBBBA permanently restored the 100% bonus depreciation deduction.

Bonus depreciation isn’t new; it was first introduced September 2001, allowing businesses to immediately expense 30% of the cost of qualifying assets purchases. Over the years, bonus depreciation was renewed and allowed to expire many times over, with deductions ranging from 30% to 100%. The OBBBA not only restores the full 100% deduction, but it also makes it a permanent feature of the tax code. Unless Congress acts to change it, businesses will be able to immediately deduct the full cost of most capital asset purchases in 2025 and in all future tax years.

20% QBI Deduction Made Permanent

The Qualified Business Income (QBI) deduction allows eligible taxpayers to deduct up to 20% of their qualified business income. This deduction was originally set to expire at the end of 2025, but the OBBBA made it a permanent addition to the tax code.

Starting in 2026, the OBBBA makes it easier for taxpayers to qualify for the full deduction. The deduction begins to phase out for individuals earning above certain income thresholds, especially for those in specified service trades or businesses (SSTBs). The OBBBA raises and expands these thresholds, allowing more business owners to benefit from the full deduction.

Finally, starting in 2026, the OBBBA guarantees that anyone with at least $1,000 of qualified business income will receive a minimum deduction of $400, even if their deduction would otherwise be fully phased out.

Raised the Interest Expense Limitation

The OBBBA made business interest more readily deductible.

Under Section 163(j) of the tax code, the maximum amount a business can deduct for interest expense is limited to the sum of:

- Business interest income,

- 30% of its adjusted taxable income (ATI), and

- Any floor plan financing interest.

The OBBBA modifies how ATI is calculated. Specifically, it restores the ability to add back depreciation, depletion, and amortization when computing ATI. This effectively increases the ATI base, which in turn raises the ceiling on deductible business interest. This ensures that many businesses, especially those with highly depreciable assets, can claim larger business interest deductions going forward.

The law made a few more changes to the business interest expense deduction limitation, specifically for businesses with foreign income and those with interest costs that are capitalized. Reach out to your CRI advisor for details.

Restored Immediate Expensing for R&D Costs

The tax law has not been favorable to research and development (R&D) expenses in recent years. The 2017 Tax Cuts and Jobs Act required that R&D expenses paid or incurred after 2021 be amortized over 60 months (or 5 years) rather than deducted immediately.

The OBBBA reversed this rule.

In a decision seen as a win for taxpayers, the OBBBA lets businesses immediately expense R&D expenses for costs incurred in 2025 and later (although taxpayers can still elect to amortize those costs over a period of at least 60 months).

Here’s where things get a bit tricky: the OBBBA lets businesses apply this rule retroactively, but only in limited circumstances.

- Most taxpayers can elect to accelerate all remaining unamortized R&D costs. They can do this in one year or over the next two years.

- Certain eligible small businesses can retroactively apply full R&D expensing to tax years 2022, 2023, and 2024. But taxpayers who choose this option will need to (1) amend those years’ tax returns, and (2) adjust R&D credits that they’ve claimed in those years.

There are many ways to change your R&D expensing strategy, so talk to your CRI advisor to determine the route that will optimize your tax position.

Expanded the Employer-Provided Childcare Credit

Beginning in 2026, the OBBBA significantly increases the employer-provided childcare credit.

Currently, employers can claim a tax credit equal to 25% of expenses incurred for providing childcare to employees, plus 10% of eligible resource and referral expenses, up to $150,000 per year. Thanks to the OBBBA, beginning in 2026, the 25% credit jumps to 40% of eligible costs, and the maximum credit allowed skyrockets to $500,000. For eligible small businesses, the credit is even higher: 50% of eligible costs and a maximum annual credit of $600,000.

What are the new thresholds that small businesses need to think about in 2025 and 2026?

Do we agree that the OBBBA provides “targeted relief” for small businesses?

In many ways, we do.

Many deductions and credits were expanded to benefit businesses, with small businesses seeing larger potential gains. However, not all changes will lower taxes on businesses. To fully grasp what changed, let’s look at the information in a new way. The following chart summarizes the changes we already discussed above and introduces a few other thresholds and limitations that changed with the OBBBA.

| Provision | OBBBA Change | Effective Date |

|---|---|---|

| Bonus Depreciation | Restores and makes permanent 100% bonus. | January 20, 2025 |

| QBI Deduction | Restores and makes permanent the 20% qualified business income deduction. Expands eligibility for high-earning taxpayers and owners of service-based businesses by raising the phase-in thresholds for deduction limitations. | January 1, 2026 |

| Business Interest Expense Deduction | Increases the amount of interest expense deductible by restoring companies’ ability to add back depreciation, depletion, and amortization to the ATI calculation. | January 1, 2025 |

| Domestic R&D Expense Deductions | Domestic research and development expenses no longer need to be amortized over 60 months. They can once again be expensed immediately. Most taxpayers can accelerate all remaining unamortized domestic R&D costs. Certain small businesses can retroactively apply full R&D expensing in 2022, 2023, and 2024 by amending prior year returns and adjusting R&D credit calculations. | January 1, 2025 |

| Employer-Provided Childcare Credit | Businesses can claim a credit of 40% (up from 25%) of the costs of providing childcare services to employees. The maximum annual credit is $500,000 (up from $150,000). Eligible small business credit is 50% of costs with maximum annual credit of $600,000 | January 1, 2026 |

| Section 179 Expensing | Raised the Section 179 expensing limit from $1.25 million to $2.50 million and the phase-out threshold from $3.16 million to $4.00 million (adjusted for inflation). | January 1, 2025 |

| Excess Business Loss Limitation | Makes permanent the $500,000 limitation on excess business losses for non-corporate taxpayers. | January 1, 2027 |

| Clean Energy Incentives | Terminates many deductions and credits sooner than originally scheduled. | January 1, 2025, or later, depending on provision |

| Corporate Charitable Deductions | Limits deduction to contributions that exceed one percent of taxable income and do not exceed 10 percent of taxable income. | January 1, 2026 |

Position Your Business for 2025, 2026, and Beyond

The OBBBA introduces some of the most significant small business tax changes in years—restoring key deductions, lifting important limits, and expanding credits that can meaningfully impact your tax posture. But it also introduces new thresholds, timing considerations, and strategic choices that require careful evaluation. Understanding how these provisions apply to your business now can help you capture new opportunities, avoid unintended consequences, and build a stronger long-term tax strategy.

If you’d like help analyzing what these changes mean for your operations, or determining which deductions and credits you can benefit from, contact your CRI advisor. Our team can help you navigate the new rules with confidence and prepare your business for the years ahead.