Entity Choice Post-OBBBA: Restructure Your Business in a Stronger QSBS

- Contributor

- Gary Pharr

May 13, 2026

The passage of the One Big Beautiful Bill Act (OBBBA) prompted many businesses to rethink their tax strategies. We’ve previously explored how the OBBBA reshaped depreciation, interest deductions, and R&D. Today, let’s revisit the Qualified Small Business Stock (QSBS) gain exclusion and see how recent law changes may increase the value for some taxpayers, depending on facts and timing.

Today, let’s do the following:

- Remind ourselves what the QSBS gain exclusion is and how it works

- Explain why eligibility for the exclusion matters to businesses and their owners

- Explore how entity choice affects QSBS eligibility

- Discuss options for changing your entity structure

- Consider potential solutions to common entity structure challenges

Quick Refresher on the QSBS Gain Exclusion

The QSBS gain exclusion under Section 1202 of the tax code encourages investment in small businesses by allowing taxpayers to exclude up to 100% of the gains they recognize when they sell qualifying small business stock (QSBS). QSBS is stock in certain qualifying US C corporations that can allow eligible shareholder to exclude some or all gains when they sell — if specific rules are met. Both the business and the investor must meet certain requirements for investors to exclude capital gains from taxable income.

Why QSBS Eligibility Matters

Businesses that qualify for the QSBS gain exclusion under Section 1202 may benefit in several ways:

- Investors could get a tax-free exit.

Investors — particularly founders and early investors — who meet all requirements may be able to exclude between 50% and 100% of the gain on share price appreciation when the business is sold (or when they sell their individual shares). - Your business may be more attractive to investors.

The potential to exclude gains is a great incentive for those who take on the risk of early investment. This perk could lead investors to evaluate your business more favorably, particularly when compared to otherwise similar companies. - Eligibility simplifies decision-making.

QSBS eligibility requires businesses to be structured and operated in a certain way. As you consider strategic moves, you’ll want to avoid decisions that could jeopardize that status. While this introduces guardrails, understanding these constraints from the get-go on can make it easier to make decisions around growth, ownership, and exit.

Why Entity Choice Determines QSBS Eligibility

The tax benefits of Section 1202 go to shareholders, but many key requirements depend on how the business is structured and operated, which is why entity choice is one of the most important factors in whether QSBS treatment is even an option.

One of the requirements to qualify under Section 1202 is that stock must be issued by a domestic C corporation. This means that businesses legally structured as sole proprietorships, partnerships, or LLCs are not eligible.

Small businesses can find this requirement to be a significant hurdle. Founders often form their businesses as partnerships or LLCs for their flexibility and for their single layer of taxation. But these structures don’t let owners take advantage of Section 1202.

Now that recent law changes have made QSBS planning more relevant for some businesses, the tradeoff is harder to ignore. Businesses should consider whether changing their entity structure could serve them and their investors better in the long run.

Changing Entity Structure to Qualify

Businesses that want to take advantage of the QSBS gain exclusion have a few structural options:

- Form the business as a C corporation from Day 1

- Convert an existing partnership or LLC to a C corporation

- Create a hybrid structure

To qualify under Section 1202, stock must be issued by a domestic C corporation — there’s no getting around it. As a result, forming the business as a C corporation from the outset is the simplest way to meet this statutory requirement.

Partnerships and LLCs can convert to a C corporation to meet this requirement, with two important caveats:

- In many cases, only growth in value after the business becomes a C corporation — and after the QSBS is issued — is eligible for Section 1202 benefits. Typically, pre-conversion appreciation won’t be eligible.

- The holding period starts once the C corporation stock is issued. Owners’ prior holding period — the time when the business operated as a partnership or LLC — does not count.

This is why many businesses explore hybrid structures.

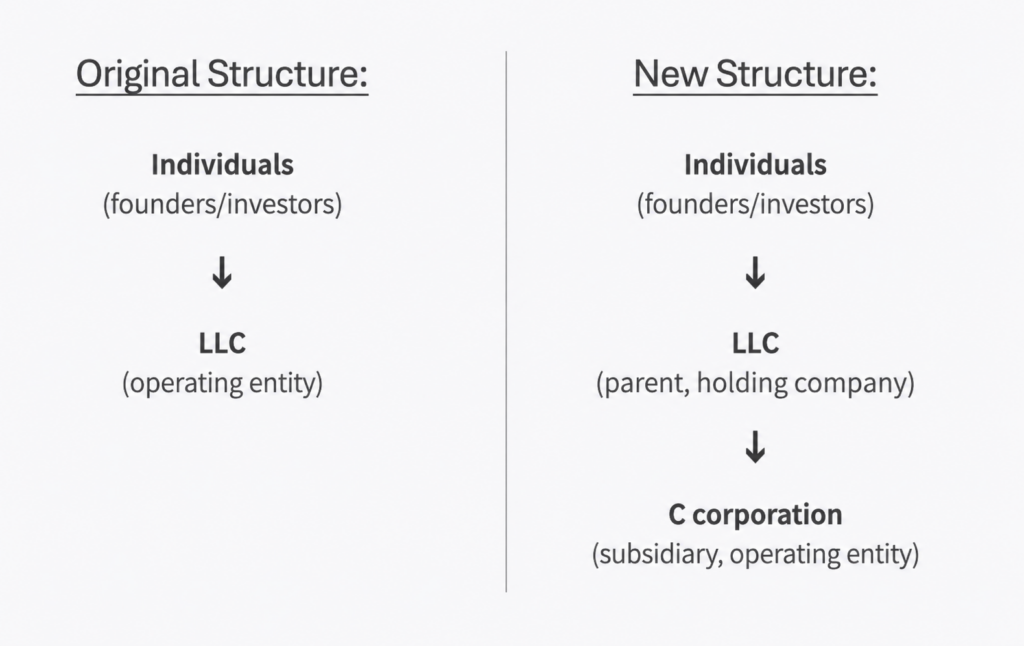

Using Hybrid Structures to Qualify an Existing Business for Section 1202

For entities already operating under a partnership or LLC structure that works for them, it can be difficult to uproot their entire business to restructure as a C corporation. Fortunately, hybrid solutions may let businesses continue to take advantage of the flexibility of the pass-through structure but still position future growth for QSBS treatment.

A common approach is to add another layer to the ownership structure:

Here’s how it works:

- The existing LLC or partnership is retained.

It continues to hold legacy assets, contracts, and operations, and owners preserve pass-through entity treatment for existing value. - A new C corporation is formed.

The entity is formed either as a subsidiary that houses operations going forward, or as a subsidiary that holds newly developed intellectual property. - The LLC contributes assets, cash, and/or intellectual property to the C corporation in exchange for newly issued C corporation stock.

The stock issuance date starts the QSBS clock (3-5 years). - The LLC owns the C corporation stock.

Partnerships and LLCs are permitted to be shareholders of qualified small businesses, which means that the QSBS gain can later flow through to the partners/members.

Of course, results depend on timing of ownership transfers and how allocations are tracked, which is why it’s important to work with an expert familiar with these tax laws to create your new entity structure.

This structure is not without its challenges, though. Changes in ownership, like admitting new members to the LLC, can complicate things.

In general, QSBS benefits may apply only to owners who were already in the LLC/partnership when it acquired the C corporation stock; new members admitted later may have different tax results, so ownership and allocations must be tracked carefully. This necessitates tight tracking of ownership, holding period, and allocations to ensure the appropriate taxpayers receive QSBS tax exclusion benefits.

Consider Your Options

Section 1202 has changed post-OBBBA, creating new planning opportunities for some businesses and owners. Businesses willing to revisit their entity structure may be able to better position themselves to take advantage of QSBS benefits, but entity changes can have other tax and legal consequences. Evaluate QSBS alongside your financing goals, administrative burden, and exit plans. Contact your CRI advisor to discuss whether your current entity structure supports your long-term tax strategy. Taking a proactive approach now may help position your business more favorably for future growth, investment, and exit opportunities.Environment